When it comes to car negotiating, car salespeople are masters in the art of diversion. Using tricky phrases or writing on paper with arrows and cross-offs, all designed to confuse you and take your mind off the bottom line - the actual purchase price of the car!

As an ex-car salesperson (or is it a reformed car salesperson?) in Phoenix, I know the tactics dealerships use for confusion and diversion - designed to get you to say "yes" to buying that shiny new vehicle for the absolute most they can get out of you!

So what exactly are these tricks and how can you counter them and keep the control in your court? That's what this article is all about. Let's get started . . .

So, you've found the vehicle you want and you're ready to start the car negotiating process. The salesman takes out a piece of paper and draws a large plus sign on it. This is called the "four square." In the first square he writes the sticker price of the vehicle. In another square he writes your down payment. Then he leaves to "talk with his manager assuring you he's going to work you the deal of a lifetime!"

After making you wait what seems like an eternity (another car negotiating tactic designed to make you anxious) he comes back with a big grin on his face and says "good news!" and puts down the paper. The remaining two squares are filled in with the trade value and payments.

This is where things quickly begin to go south in the car negotiating process. The trade value is usually WAY TOO LOW and the payments are WAY TOO HIGH.

Don't be fooled! This car negotiating tactic is designed to throw you off balance and make you think the payments you want are not obtainable, that you have overestimated the value of your trade-in, so you'd better rethink the down payment or monthly payments. It's a subtle way to manipulate you into doubting yourself and becoming anxious.

The salesman's job at this point is to get a signed commitment "bumping" you up from the original down payment and payments you want. Here's how he does it:

You're looking at his sheet and getting nervous thinking you can't afford this vehicle! Then he asks you, "What payments were you hoping to get?" Or "What were you thinking your trade-in was worth?" These phrases are designed to plant doubt in your mind. Maybe what you thought your trade-in was worth more than it is . . . Maybe the payments you want are not reasonable for this vehicle . . . maybe you need more money down.

For instance:

He says your payments are $700 and you wanted $500. You think you're miles away so you say to yourself, "Well . . . . I can afford $570 if I budget myself." So, already you've come up a bit more than you already wanted.

Also, during this phase of the car negotiating process he's taken your focus OFF the primary goal - the PRICE of the vehicle you want to purchase! Now, instead of talking "purchase price" - which translates into less profit for him, he's got you looking at "payments" - which translates into more profit for him because he can control those through stretching the term or changing the interest rate, without touching the value of the car you want to purchase!

Taking the "four square" sheet he writes down $570, then asks the next question "Up To?" Meaning, $570 to $600 maybe? So, the salesman writes down something like "I will buy and drive right now for $570 to $600 a month" and asks you to sign it. Then he goes back to "talk to his manager." So you see, already he's bumped you up by $100 a month, and hasn't even discounted the vehicle yet!

You're thinking, well, to get to that payment he's going to have to come up in trade value (which is usually about $1,000 to $2,000 more than he quoted you) or come down in price (which is a last resort). But even if he comes up in trade value, he's low-balled you on it anyway, so he still hasn't LOST any real profit. And the truth is, YOU haven't even begun car negotiating because HE is controlling the entire situation!

After waiting another eternity he comes back with more "Good News!" He's gotten his manager to increase your trade-in (or discount the car) by $1,000! Wowee! This lowers your payments down to $675! And it's all written nicely on the four square sheet and circled and initialed by the manager, to look official.

At this point you're getting tense and a little overwhelmed. You state that you just can't afford that payment and start to get up. The salesman sees his commission going out the window and stops you. He says, "If I could get the payments around where you want them will you buy the vehicle?"

Listen to the words again, "around where you want them." In car negotiation-speak this translates into about $35 to $50 more than you've already committed to.

At this point he whips out his sharpie pen and starts drawing circles. Saying things like, "well, to get payments around where you need them we need to come up in trade or down in price. I need to talk to my manager and see what he is willing to do to sell this vehicle. Obviously we're a long ways apart."

Here he'll start drawing arrows from payments to trade-in, etc. He'll write down your payment ($600, NOT $570) and then he'll circle it, and cross it off (subtle implication, don't count on it buster).

This is where the second "bump" comes in. He'll say, "If I can get my manager to come up in trade or down in price, can you come UP in down payment? Remember, each $1,000 down equals about $25 in payments."

Once again, focus is OFF the price of the car and ON the payments, which can be controlled through interest rates and stretching them out! You're still at or around full sticker AND your trade has been undervalued by probably $1,000 (still), and you're growing more tense by the minute! Which hampers your ability to focus in on the car negotiating process.

So you say, "well . . . we can give you an additional $1,000 if we eat dog food for a month." And he writes that down.

Then he scribbles another "commitment" on the paper and asks for your signature. By now the "four square" is looking a little ragged with numbers and arrows and slash marks everywhere. You're thoroughly confused and tense thinking that maybe you can't afford this car - and you really want it!

In terms of car negotiating he's got you right where he wants you. He's bumped you up in monthly payment, up in down payment, he's still holding back on the trade value (if it's worth $2,000 and he gives you $1,000 - that's considered an additional $1,000 profit for him too), AND he hasn't touched or only slightly touched the price of the car!

I could go on and on and on about these car negotiating tactics. Suffice it to say, they are designed to confuse you, make you think you can't afford the vehicle with the money you've got down or payments you want, sell you the vehicle for it's full price and steal your trade for less than it's really worth.

At some point a sales manager steps in and pressures you to increase your down payment or monthly payments also. And by this time you're tense, excited, nervous, and who knows what else!

So, how do you keep the ball in your court and control the situation?

First and foremost - Get pre-approved for a vehicle loan! This is the easiest way to take the wind out of their sales. When you are pre-approved it puts you in the drivers seat because YOU control the negotiating on the price of the vehicle and your trade-in. Pre-approval also helps you when looking for a vehicle by keeping you in check and not honing in on a vehicle that is realistically more than you can afford.

Shop online first! Better yet, get pre-approved from a lender who will connect you with a dealership. This way you'll be working one-on-one with a single salesman and he'll know up-front what you can afford and help you accordingly.

Know your trade-in value. Visit Kelley Blue Book, Edmunds, or check out your local Auto Trader to see what similar vehicles are selling for. Then hold them to that value no matter what! Often lenders who pre-approve you will also give you a good estimate of your trade-in value to help you when car negotiating.

Once pre-approved, don't let the dealer talk you into "pulling your credit to see if he can get you a better interest rate." Once again, this puts the ball in their court because with another lender perhaps they can lengthen payment terms and lower your monthly payments without discounting their vehicle.

Shop with a friend or someone who is a good negotiator. Then - listen to them when they give you advice about what to do or say!

Car salesmen are professionals in the art of confusion. Don't become one of their victims! Pay attention to the words they say and their tactics that confuse and manipulate. Keep your eye on the prize . . .the best possible price for that shiny new vehicle you want!

As a former top 5 car salesperson in Phoenix, AZ Leslie Kearney is an expert in car negotiation and auto financing. As the founder of [https://www.1-800BadCredit.com] she provides help and solutions to people with bad credit or no credit.

Related: Negotiations Classes

Free Downloads

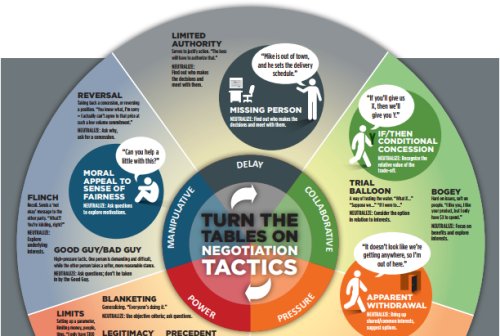

Neutralizing Negotiation Tactics

Public Negotiation Training